The Indian Rupees Trading higher At 85.37 against the Dollar

Share

Financial Market Overview

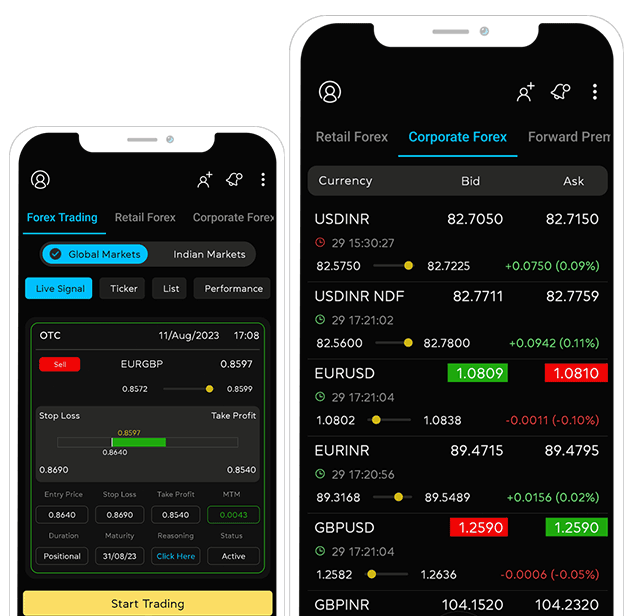

USDINR

The Indian rupee opened stronger at 85.3150 against the U.S. dollar on Friday, compared to its previous close of 85.3325 on Thursday. The Indian rupee opened stronger on Friday, supported by broad-based U.S. dollar weakness after softer U.S. economic data reinforced expectations of Federal Reserve rate cuts later this year. Despite a brief boost from the India-Pakistan truce, the rupee remains weaker on the week and has underperformed regional peers. A Mumbai-based trader noted that the USD demand has shifted the rupee’s bias from positive to neutral in the near term. The dollar index dropped as U.S. retail sales control group declined 0.2% MoM and factory output fell 0.4% in April. Additionally, PPI inflation dropped 0.5%, raising the likelihood of at least two Fed rate cuts in 2024. U.S. Treasury yields also fell in response.

United States 10-Year rates were 4.424% on the bond markets, while 2-year Treasury yields were 3.947%. The DXY index trading around 100.63.

At the time of writing, the USDINR was trading at 85.37/85.38.

GBPUSD

The GBPUSD pair edged lower on Wednesday, hovering just below the 1.3300 mark as markets absorbed mixed but largely balanced economic data from both the UK and US. UK Q1 GDP surprised to the upside, rising 0.7% QoQ and signaling stronger economic momentum. Meanwhile, US PPI inflation eased to 0.1% MoM in April, calming concerns over cost pressures and tariff impacts. The combination of upbeat UK growth and soft US inflation kept the pair within a narrow consolidation range. Attention now turns to Friday’s release of the University of Michigan’s Consumer Sentiment Index, which is expected to rebound slightly to 53.4 from a two-year low of 52.2. A better-than-expected print could offer fresh direction for the greenback.

At the time of writing, the GBPUSD was trading at 1.3316/1.3318.

EURUSD

EURUSD saw volatile movement on Asian session on Friday, briefly touching the 1.1000 level for the second time this week before rebounding to near the 1.1200 mark. The euro came under pressure after Eurozone Q1 GDP slipped to 0.3% QoQ, though annual growth held at 1.2%. The soft quarterly print gave traders reason for caution. In the US, PPI inflation cooled to 0.1% MoM in April, easing immediate concerns about tariff-driven price pressures. Eyes now turn to Friday’s University of Michigan Consumer Sentiment Index, with expectations for a modest recovery to 53.4 from 52.2. A stronger reading could support the USD, potentially adding fresh directional cues for the EURUSD pair.

At the time of writing, the EURUSD was trading at 1.1204/1.1205.

USDJPY

The Japanese Yen (JPY) extended its winning streak for the fourth consecutive session on Friday trading around 145.30, hitting a fresh weekly high against the US Dollar (USD) during Asian trading. Despite a weaker-than-expected Q1 GDP print, the JPY remained strong amid rising expectations of another Bank of Japan (BoJ) rate hike. Progress in US-Japan trade talks further boosted sentiment. These supportive factors outweighed the recent market optimism driven by easing global trade tensions, which had dampened demand for safe-haven currencies. Meanwhile, the USD remained under pressure as cooling inflation and weak consumer spending reinforced expectations of Fed rate cuts. The growing policy divergence between a hawkish BoJ and a dovish Fed continues to favor the JPY, keeping bullish momentum intact.

At the time of writing, the USDJPY was trading at 145.28/145.29.

Share

Recent Blog

Want to manage Forex?

Newsletter signup

Receive forex updates right in your mail box or Whatsapp

Newsletter Subscribed

Download the Myforexeye App to get latest market updates, live rates, forward rates and much more.