Morning Session – Indian Financial Market (16 Mar 2026)

Share

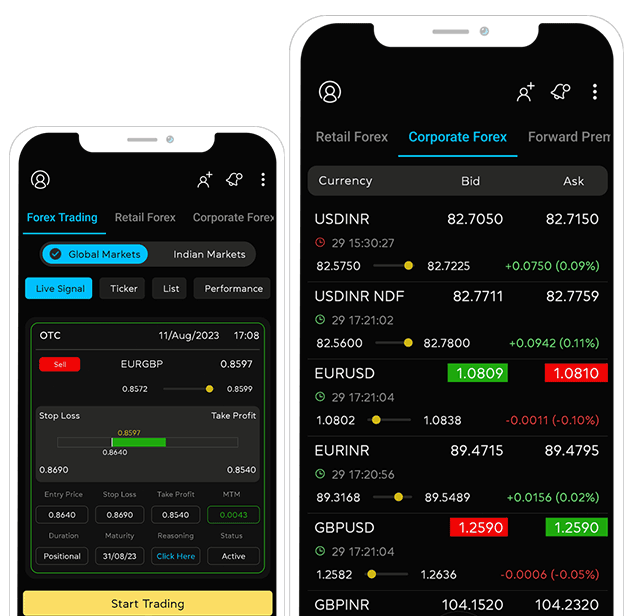

Indian Rupee

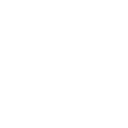

The Indian rupee opened at 92.43 against the U.S. dollar on Monday, compared to its previous close of 92.4550 on Friday. The Indian Rupee (INR) ended its four-day winning streak against the US Dollar (USD) on March 16, 2026, with the USDINR pair opening lower around 92.80 amid a pause in the Greenback's rally and speculation that the Strait of Hormuz—through which about 20% of global oil flows—might reopen soon. This optimism stems from US President Donald Trump's statements on Truth Social, where he claimed positive responses from several nations (including China, France, Japan, South Korea, and the UK) to join US-led efforts in sending warships to secure and reopen the strait, which has been disrupted amid the ongoing US-Israel-Iran conflict and Iran's retaliatory closure threats. However, the impact on oil prices has been limited so far, with gains surrendering, though higher crude remains a headwind for India as a major oil importer; notably, Iran has permitted some Indian-flagged tankers (carrying LPG) safe passage recently, easing immediate supply fears. Despite this relief, the INR's broader outlook stays weak due to persistent foreign institutional investor (FII) outflows from Indian stocks—net sellers every day in March, offloading over Rs. 56,883 crore—and upcoming domestic data like February's Wholesale Price Index inflation (expected at 2%). Technically, the pair holds a bullish bias above the rising 20-day EMA near 92.00, with RSI overbought but no reversal yet, supporting potential upside toward 92.97 and 93.50 if resistance breaks, while support lies at 92.00 and deeper at 91.30.

Indian Equities

The Indian stock market exhibited volatility on March 16, 2026, with benchmark indices Sensex and Nifty 50 fluctuating between modest gains and losses amid mixed global cues and persistent investor caution. Key concerns driving sentiment included the ongoing US-Iran war (now in its third week since late February 2026), which has disrupted global oil supplies by effectively halting traffic through the Strait of Hormuz, keeping crude oil prices elevated above $100 per barrel (Brent around $103–104). This has fueled inflationary fears, weakened the Indian rupee to near-record lows around 92.43 against the US dollar, and prompted heavy FII outflows. Asian markets traded mixed, while US indices closed lower the previous week on oil supply worries. Domestic highlights featured sharp moves in select stocks, such as Bajel Projects surging 13% on a major transmission contract win, VA Tech Wabag up 5% after securing a Chennai water project, Adani Power rising over 4% on a power supply order, but IDBI Bank crashing 15% amid reports of scrapped government divestment plans. Analysts noted high volatility, with Nifty hovering near critical support levels around 23,000 (potential bounce to 23,600+ if held, or further drop toward 22,000 if breached), advised caution or selective buying in resilient sectors like pharmaceuticals and telecom, and highlighted gold prices easing but remaining supported by geopolitical risks. Overall, uncertainty from the prolonged Middle East conflict, high energy costs, and foreign fund selling continued to dominate market dynamics.

Indian Government Bonds

The Indian rupee and government bonds are expected to remain under pressure this week due to the ongoing Iran war, which has disrupted global energy supplies and driven oil prices above $100 per barrel through military actions affecting key routes and facilities like Kharg Island. The rupee recently touched a record low of 92.4750 against the dollar, largely stabilized by Reserve Bank of India (RBI) interventions, while foreign investors have pulled out over $5.5 billion from Indian stocks in March amid risk aversion toward emerging markets. Goldman Sachs analysts now forecast the rupee weakening further to 95 over the next 12 months, citing a severe terms-of-trade shock from elevated energy costs impacting trade, supply chains, and remittances. On the bond side, the benchmark 10-year yield closed at 6.6798%, supported by substantial RBI purchases—including a record 572.10 billion rupees in early March—to anchor the market despite oil-driven confidence erosion; traders see yields ranging between 6.62% and 6.72% ahead, though overnight index swaps indicate hedging against potential imported inflation, even as analysts doubt a major policy reversal unless external pressures intensify significantly. Key upcoming data includes India's February WPI inflation and various U.S. economic releases, which could add further volatility.

The 10-year benchmark bond yield was trading at 6.701%.

Share

Recent Blog

Ready to make smarter forex decisions?

Get timely market updates straight to your inbox and WhatsApp.