Morning Session – Indian Financial Market (12 February 2026)

Share

Indian Rupee

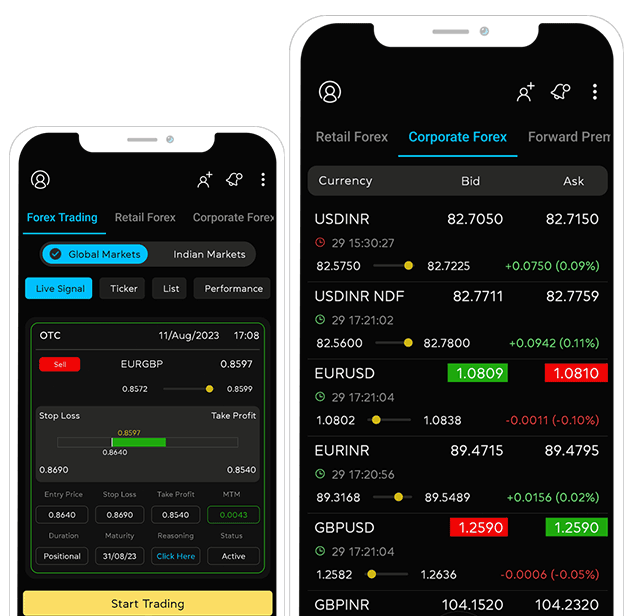

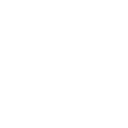

The Indian rupee opened at 90.4650 against the U.S. dollar on Thursday, compared to its previous close of 90.71 on Wednesday. The Indian Rupee strengthened on Thursday, pushing USD/INR lower despite elevated US Treasury yields following stronger-than-expected US jobs data. Asian currencies remained largely stable, with traders suggesting RBI intervention supported the Rupee's opening, while a bank trader noted that neither the recent US–India interim trade framework—aimed at tariff reductions, energy cooperation, and significant Indian purchases of US goods—nor the latest US employment figures (130,000 Nonfarm Payrolls in January, beating expectations) materially altered the Rupee's trajectory, as its sensitivity to external factors has diminished. The currency drew further backing from equity inflows and broad US Dollar weakness, though corporate demand for dollars may limit gains. Meanwhile, the US Dollar Index hovered near 96.80, with markets now pricing a 94% chance of the Fed holding rates steady at its next meeting (up from 80%), shifting focus to the upcoming CPI report; expectations point to potential rate cuts starting in June, even as Fed officials emphasized data-dependence and persistent inflationary risks.

Indian Equities

The Indian stock market witnessed a decline on February 12, 2026, with the Sensex falling around 327 points (0.39%) to 83,907 and the Nifty dropping 86 points (0.33%) to 25,867 by mid-morning, primarily driven by sharp selling in IT stocks. The Nifty IT index plunged over 4%, with major losers including Tech Mahindra, Infosys, and Wipro (down up to 5%), as fading hopes of a near-term U.S. Federal Reserve rate cut—following stronger-than-expected January jobs data—and persistent concerns over AI-driven disruptions to traditional IT business models weighed heavily on sentiment. Rising crude oil prices (Brent at ~$69.72 per barrel) added pressure due to potential inflationary and trade deficit risks for oil-importing India, while weak global cues from lower U.S. closes and Asian markets contributed to the downturn. Despite the pullback, Nifty remains in an uptrend above key averages, with support near 25,700–25,780 and resistance around 26,000.

Indian Government Bonds

Indian government bonds are expected to surrender some of their recent gains in early trading on Thursday, influenced by a rebound in US Treasury yields following stronger-than-expected US jobs data, which showed non-farm payrolls rising by 130,000 in January—well above economists' forecasts of around 70,000 and up from a revised 48,000 in December—reducing near-term expectations for Federal Reserve rate cuts. A trader from a private bank anticipates the 10-year benchmark Indian government bond (6.48% 2035) yield to trade in the 6.70%-6.75% range, after closing at 6.7088% on Wednesday, down 5 basis points over the prior two sessions. While a bullish sentiment persists from Wednesday's response to state debt developments, major movements are unlikely until the release of January's domestic inflation data later in the day, which a Reuters poll expects to show consumer inflation rising to 2.4%—still within the RBI's 2%-6% target band—and marking the start of a new CPI series based on 2024 prices. Overnight index swap rates in India are also likely to rise in tandem with global yields.

The 10-year benchmark bond yield was trading at 6.723%.

Share

Recent Blog

Ready to make smarter forex decisions?

Get timely market updates straight to your inbox and WhatsApp.