Morning Session – Indian Financial Market (12 December 2025)

Share

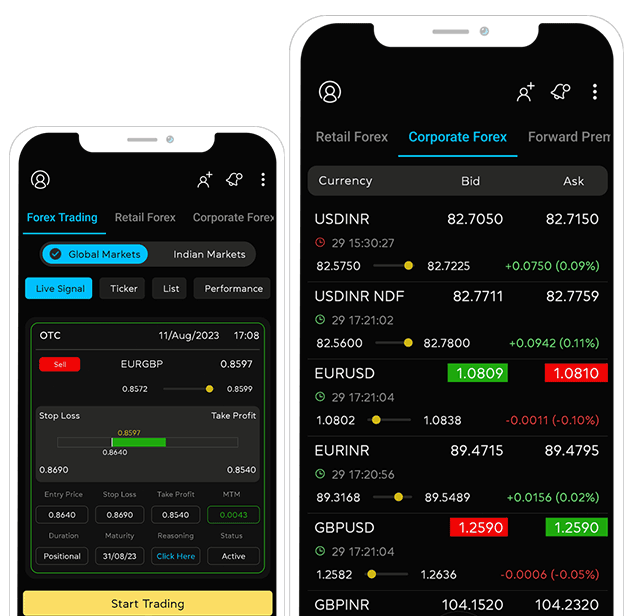

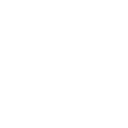

Indian Rupee

The Indian rupee opened at 90.4325 against the U.S. dollar on Friday, compared to its previous close of 90.3675 on Thursday.. The Indian rupee’s sharp decline in 2025, now Asia’s worst-performing currency with a 5% drop against a weakening dollar and breaching the psychologically important 90 level, is evoking memories of the 2013 “Fragile Five” crisis, though the underlying causes differ markedly. Unlike 2013, when runaway inflation, a gaping current-account deficit, and an overheated economy triggered by politically driven rate cuts led to a brutal sell-off, today’s India enjoys near-zero inflation, a manageable external position, and strong services exports; the rupee’s weakness is instead acting as a buffer against steep 50% U.S. tariffs and delayed trade deals. However, heavy foreign equity outflows of $17 billion amid disappointing corporate earnings and sky-high valuations, surging gold (and crypto) imports fueled by global rallies and low local yields, and excessively high real interest rates (over 6%) are draining dollar liquidity and echoing the capital-flight dynamics of twelve years ago. With the RBI appearing reluctant to ease further and holding large net dollar short positions, markets are growing anxious about a potential slide toward the politically toxic 100 level, especially if President Trump’s unpredictable tariff threats and on-again-off-again negotiations drag into 2026, turning today’s controlled depreciation into a new test of Governor Sanjay Malhotra’s resolve.

Indian Equities

Indian equity benchmarks Sensex and Nifty 50 are set to open firmly higher on Friday, December 12, 2025, with Gift Nifty futures trading around a record 26,134 (up 108 points), after the US Federal Reserve delivered an expected 25 bps rate cut and signalled a less hawkish path ahead, sending the Dow Jones up 646 points (1.34%) and the S&P 500 to a fresh all-time closing high while the Nasdaq dipped slightly on tech weakness. Domestic markets had already snapped a three-day losing streak on Thursday with solid gains in auto and IT stocks, buoyed by falling US 10-year yields and hopes of slower FII outflows. Positive global cues continued into Asia, where Australian shares rose nearly 1%, while a sharply weaker US dollar (hitting multi-month lows), rebounding oil prices, a surprise narrowing of the US trade deficit, and an upbeat Modi-Trump phone call discussing accelerated trade and technology cooperation added to the bullish mood; even as gold eased slightly from seven-week highs and markets braced for a likely Bank of Japan rate hike next week, sentiment remains risk-on heading into the Indian session.

Major gainers on Nifty are LT, Tata Steel, Hindalco, JSW Steel, BEL, Ultra Cement Co, Indigo, Adani Ports, Axis Bank and losers are Infosys, Wipro, Max Health, Bajaj Auto, HCL Tech, Tech Mahindra.

Indian Government Bonds

Indian government bonds are likely to open largely unchanged on Friday, December 12, 2025, with the benchmark 10-year yield expected to trade in a narrow 6.55–6.60% range after closing at 6.5832% the previous day, as traders brace for a ?280 billion auction of 15-year and 40-year paper that will test whether Thursday’s sharp rally—triggered by a less-hawkish-than-feared US Fed 25 bps rate cut and aggressive RBI bond buying under open market operations—has lasting momentum. While record-high central bank purchases this fiscal year and hopes of inclusion of the liquid 6.33% 2035 bond in next week’s OMO lent support, sentiment remains cautious after foreign investors unwound receive positions earlier in the week on bets that India’s easing cycle is over, pushing overnight index swap rates higher; with fresh supply looming and demand-supply balance turning unfavourable, the auction outcome will be the key focus for the day.

The 10-year benchmark bond yield was trading at 6.559%.

Share

Recent Blog

Newsletter signup

Receive forex updates right in your mail box or Whatsapp