Indian Rupee Finished The Day at 91.9825

Share

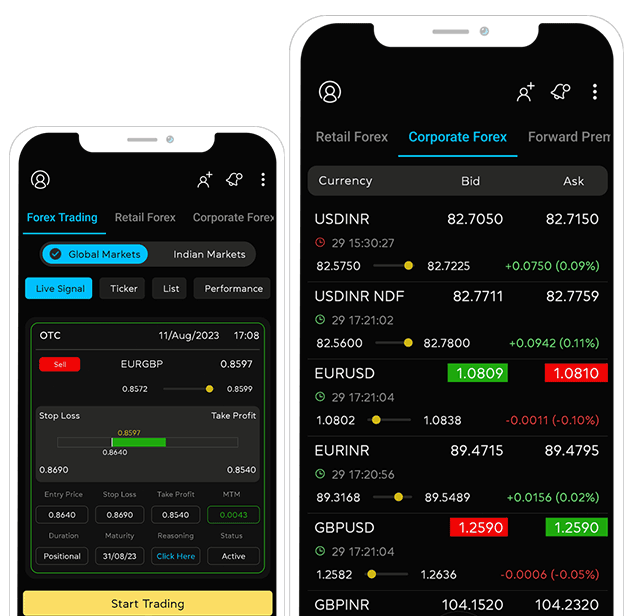

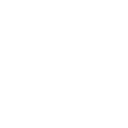

The Indian rupee closed at 91.9825 on Friday in comparison to its previous closing at 91.9550 on Thursday evening. The USDINR pair is surging toward record highs, recently hitting 92.51 on Wednesday amid a weakening Indian Rupee driven by weak Asian risk sentiment, dollar buying tied to NDF maturities, chronic demand-supply imbalances, bullion imports, equity outflows, and slow exporter hedging. The pair hovers around 92.00–92.10, maintaining a bullish bias within an ascending channel on the daily chart, with the RSI near overbought levels signaling strong momentum; resistance looms at the recent peak of 92.51 (potentially targeting 93.60), while support sits at 92.00 and lower EMAs. This INR depreciation aligns with broader US Dollar strength, fueled by reaffirmed commitment to a strong dollar policy from Treasury Secretary Scott Bessent, speculation over President Trump's impending nomination of hawkish former Fed Governor Kevin Warsh as the next Federal Reserve Chair (to be announced soon), and the Fed's recent decision to hold rates steady amid resilient growth and elevated inflation. The RBI continues to act as a key backstop against breaches beyond psychological levels like 92.00, while economists anticipate no policy rate changes from 5.25% through 2026.

At close, the Sensex was down 296.59 points or 0.36 percent at 82,269.78, and the Nifty was down 98.25 points or 0.39 percent at 25,320.65. Hindalco, Tata Steel, Coal India, ONGC, ICICI Bank were among major losers on the Nifty, while gainers were Tata Consumer, Apollo Hospitals, Nestle, M&M, ITC.

Indian benchmark indices ended lower, snapping a three-day winning streak amid caution ahead of the Union Budget on February 1 (with markets open for a special Sunday session). The Sensex closed down 296.59 points (0.36%) at 82,269.78, while the Nifty settled 98.25 points (0.39%) lower at 25,320.65, dipping below the 25,350 mark. Metal stocks led the decline with the Nifty Metal index plunging around 5% due to profit booking after recent surges and easing commodity prices (e.g., sharp corrections in copper, silver, zinc), dragging major losers like Hindalco, Tata Steel, Hindustan Zinc, Vedanta, and NALCO. Other sectors such as oil & gas, banking, IT, and energy fell 0.5-1%, while defensive pockets like FMCG, pharma, media, and consumer durables gained 0.5-1.8%, with top Nifty gainers including Nestle, Tata Consumer, Apollo Hospitals, M&M, and ITC. Broader markets were mixed, with the Midcap index down marginally and Smallcap up slightly. Analysts cited mixed global cues, rupee weakness near record lows (closing around 91.99/USD), persistent FII outflows, rising geopolitical risks, higher oil prices, and pre-Budget positioning as key pressures, though some recovery occurred intraday on value buying and positive Economic Survey GDP projections (6.8-7.2% for FY27). Market sentiment remained subdued with expectations of volatility during the Budget session.

Share

Recent Blog

Ready to make smarter forex decisions?

Get timely market updates straight to your inbox and WhatsApp.